How I’m Building a SpaceX Position Below the IPO Price Using Options

I didn’t get SpaceX at the IPO price — so I built an options strategy designed to lower my cost basis, create flexibility, and let me accumulate shares over time.

When SpaceX opened at $135 per share, I wasn’t able to get shares at that price. Instead of chasing the stock after the move, I started thinking about how I could build a position more intelligently — one that let me participate now, lower my effective cost basis, and give myself room to manage the trade over time. That’s what this strategy is about. It’s not a quick flip, and it’s not a one-day trade. It’s a structured options campaign designed to help me own SpaceX on better terms. Source

My goal here is not to predict every short-term move. My goal is to build a long-term position in a company I want exposure to, while using options to shape both the entry and the risk. I’m treating this like a campaign, not a lottery ticket. That means starting with a small share position, selling premium where I’m comfortable taking assignment, and using structure to create flexibility on both the upside and downside.

Why I Started With Shares — But Not Too Many

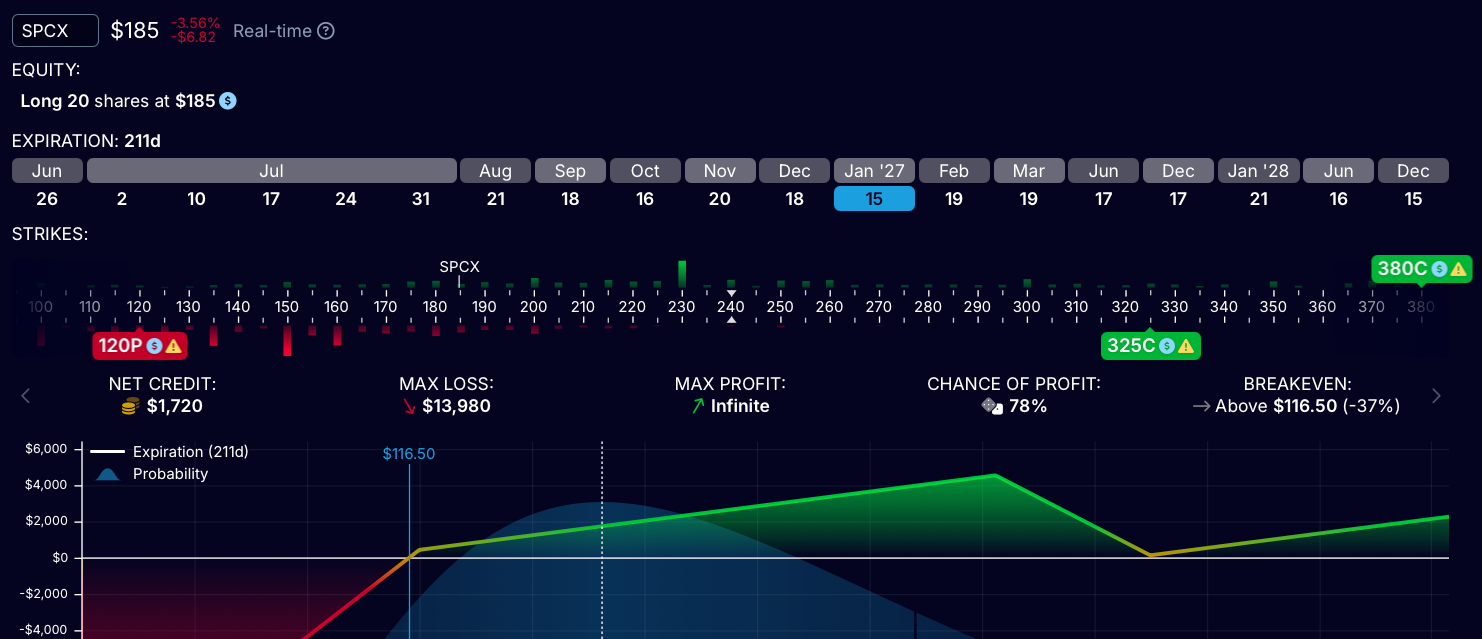

The first thing I’m doing is buying 20 shares of SpaceX. That’s not a huge position, and it’s not meant to be. I wanted enough exposure so I wouldn’t completely miss the move if the stock kept running, but not so much that I’d be overcommitted right out of the gate. Early IPO-style price action can be volatile, and I expect there to be pullbacks, lockup-related pressure, and plenty of noise along the way. Starting with 20 shares gives me a foothold without forcing me to go all in too early.

That smaller entry also reflects my time horizon. I’m not trading this for next week or next month. I’m thinking in terms of five to ten years. If there’s a pullback, I want to be in a position to add. If the stock keeps ripping higher, I can continue to build the position over time while using options to reduce my cost basis. Either way, I want the structure to work with me, not against me.

The Core Idea: Get Paid While I Build the Position

On top of the 20 shares, I’m also selling a $120 put. That means if SpaceX drops below $120, I’m obligating myself to buy 100 shares at that price. For me, that’s not a problem — that’s part of the plan. If I’m going to own more SpaceX, I’d rather get paid while I wait and only take assignment at a level I’m comfortable with. I framed this as using options to lower the price at which I ultimately build the position.

At the same time, I’m putting a call spread over the top of the trade using the January 2027 expiration, with strikes at $325 and $380. The reasoning is simple. I want upside participation from the current price up to the $325 area, and I’m willing to cap part of the extreme upside beyond that in exchange for premium that helps fund the position. I chose $380 because it was the highest available strike in that expiration, and pairing it with the $325 short call gave me a structure I could live with.

Why I’m Willing to Cap Some Upside

A lot of people hate the idea of limiting upside, especially in a name with the kind of story SpaceX has. I understand that. But the whole point here is that I’m not trying to build the perfect fantasy trade — I’m trying to build a trade that improves my real-world entry. If I can use premium from the short put and the call spread to materially reduce my cost basis, that tradeoff is worth it to me. I still get meaningful participation if the stock climbs, and I give myself more room to manage the position instead of just hoping I bought at the perfect time.

I also made the point that if the stock really starts to run, I’m not locked into doing nothing. I can roll the structure, move strikes, extend time, or close pieces of the position early. That’s one of the biggest advantages of thinking like an options trader instead of a passive holder. I’m not just buying and praying. I’m building a framework I can actively manage.

How the Premium Changes the Math

One of the reasons I like this setup is that the premium meaningfully offsets the cash outlay. In the video, I walked through how the option premium taken in reduces the effective cost of entering the initial 20-share position. That doesn’t mean the shares are “free,” and I was careful to say that. There is still real risk here. But it does mean I’m using the options market to improve my economics instead of simply accepting the quoted share price as my only path in.

That’s really the heart of the whole trade. If I’m willing to own more shares lower, then selling the put pays me for that willingness. If I’m willing to cap some upside in a defined range, the call spread pays me for that too. Together, those premiums reduce the amount of cash I have to commit up front and help drive down my effective basis in the shares I already bought.

The Risk Is Real — I’m Just Choosing It Deliberately

I also spent time in the video walking through what could go wrong, because that matters. If the 20 shares go to zero, I lose on those shares. If I get assigned on the $120 put, I’m committing more capital to the name. And if the stock lands in an awkward zone relative to the call spread, there can be friction on the upside that I have to actively manage. None of that is hidden. This is not a risk-free strategy, and I’m not pretending otherwise.

What I am saying is that these are risks I’m consciously willing to take because they line up with what I want. I want long-term exposure. I’m comfortable buying more at $120. And I’m comfortable sacrificing some upside smoothness in order to reduce my cost basis and create a more manageable structure. Risk doesn’t disappear in options trading — it gets shaped. My goal is to shape it into something that matches my time horizon and conviction.

Why Time Is a Feature, Not a Bug

One of the most important parts of this setup is the use of time. I’m not putting on a structure that expires in a few weeks. I’m giving this trade runway into January 2027. That matters because it gives the thesis room to develop and gives me more chances to make adjustments. It also means the position isn’t entirely binary. There’s time value in the options, and that creates opportunities to manage winners, cut risk, and roll exposure before expiration becomes the only thing that matters.

In the video, I used the charting and modeling tools to show how the payoff shape changes over time. Close to expiration, the trade looks more rigid. Farther away from expiration, it’s smoother, more flexible, and easier to manage because there’s still extrinsic value left in the structure. That’s one of the reasons I prefer this style of campaign: it gives me room to participate and room to think.

How I Plan to Manage It

If SpaceX never gets up to the short call area, I can let pieces of the structure decay, keep the premium, and then reset into a new position. If the stock shoots higher, I can buy back pressure points, push strikes farther out, or roll the trade into later expirations. If it pulls back, I may get the chance to add inventory at a price I already decided I like. In every case, the trade is built to keep me involved instead of forcing a one-time decision.

That’s why I think of this as a campaign. I’m not trying to nail one price target and walk away. I’m trying to create a repeatable process: buy a little, sell premium, add strategically, roll when necessary, and continue building toward a larger long-term position. Over time, if the thesis stays intact, I can keep using premium to accumulate more shares and improve the overall basis.

Final Thoughts

The big picture here is simple: I missed the IPO price, but I didn’t miss the opportunity. Instead of chasing the stock, I built a structure that lets me participate now, potentially buy more lower, and manage the trade if SpaceX moves hard in either direction. For me, that’s a much better way to approach a speculative long-term name than just throwing capital at the screen and hoping for the best.

This is how I think about options when they’re used well. They’re not just leverage tools. They’re planning tools. They let me decide in advance what kind of buyer I want to be, what kind of risk I’m willing to take, and how I want to respond if the market gives me a better opportunity later. That’s the framework behind this SpaceX trade, and it’s the reason I’m comfortable building it this way.